Specialty Telecommunications – Wireless Infrastructure Contractors

A Middle Market M&A Update—January 2014

By: Steve Mooney

Industry Snapshot

The $16.4 billion¹ per year specialty contractor industry provides outsourced construction engineering, installation, maintenance and repair for major telecommunications firms (e.g. AT&T, Verizon, T-Mobile, Sprint), regional utilities (e.g. PG&E, Duke, FPL, TXU, Con Ed) and the pipeline industry (e.g. TransCanada, Piedmont Natural Gas, Xcel, Lone star). Over several decades these industries have turned to specialized contractors for their highly skilled and flexible workforces to engineer, construct and mange their underlying infrastructure.

The focus of this report is primarily on the wireless telecommunications infrastructure sector. The wireless carriers continue to experience massive demand for data capacity on their networks. This demand is driven by the explosive growth for mobile broadband services (i.e. smartphone, tablet and other devices, etc.) with an estimate of over 225 million active devices in service today with net adds growing at 20% per annum². To manage this shift from traditional voice to high speed data services, the carriers are completing upgrades of their networks to 4G LTE. In the macro network, the 4G LTE technologies require smaller and more dense tower facilities. The CTIA estimates the number of cell towers have increased from approximately 135,000 in 2010 to over 242,000 as of October 2013

Growth in Small Cell Networks

Furthermore, the escalating demand for wireless services has caused carriers to begin offloading mobile traffic from their macro networks to preserve available spectrum through small cell and distributed antenna systems (DAS) deployments. These cells offer low powered radio access with a range from 10 to 200 meters; using clusters of smaller transmitters at a site, thereby boosting capacity and coverage and reducing ‘dead zones.’ These networks were originally deployed in high density event venues (e.g. hospitals, arenas and stadiums) but have evolved into core access technologies in commercial buildings or in outdoor applications where cell towers are impractical or prohibited by local ordnance.

Opportunity in Wireless Carrier Market

Lightwave Media estimates the total 2014 capital spending by the US carriers on their wireless networks will be in excess of $31 billion² as they to continue the expansion of both their macro cell and micro-cell 4G LTE networks. Verizon and AT&T of course, represent the preponderance of these outlays. We estimate that engineering and construction is roughly a $7 billion sub-segment, growing at a 15% to 18% annual rate through 2016. The remainder represents the cost of towers, equipment, backhaul as well as internal project resources.

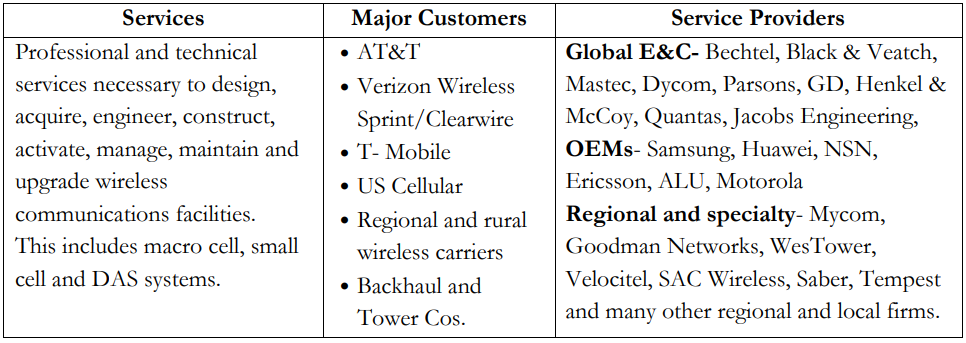

This segment includes the following outsourced services, major customers and the major service providers:

Verizon Wireless has largely completed its national 4G LTE macrocell network in 2013 and is now focused on what it calls its LTE2C small and microcell network. Our industry contacts indicate AT&T Wireless is as much as 12 to 18 months behind VZW because of the delays caused by the 2011-12 aborted attempt to merge with T- Mobile. AT&T Mobility is also active in implementing small and microcell technologies on a selective basis. With the recent $4 billion investment from Softbank we expect Sprint to be accelerate its capex in 2014 through 2016 to coincide with its integration with Clearwire.

In general, we see no let up in the capex through 2016 given what appears to be unquenchable demand for multi megabit up to gigabit data speeds and the re-engineering of the carrier networks to move traffic off the macro networks toward small cell, microcell, DAS and even WIFI access networks.

Trends Affecting Specialty Wireless Infrastructure Players

Traditionally, the carriers constructed and maintained their infrastructure through a series of national contracts (i.e. Turf Contracts) with relatively small number of large well-capitalized E&C firms such as Bechtel and Black & Veatch. These prime contractors often managed dozens of small local “mom and pop” sub contractors. As the technical and operational complexity of rolling out 4G LTE and small cell technology multiplied, centralized management of these programs became untenable. As a result, deployments fell behind schedule and cost overruns exploded for the major carriers. There was also a lack of accountability and visibility into the 4G deployment programs. As a result, there is an industry wide shift toward more direct contractor relationships and less dependence on large program management contracts. The following are key trends and demands from the national carriers:

• Ability to “Self-Perform.”— Driven by delays and cost overruns as a lack of accountability, the carrier customers are demanding their vendors bring the management, technical and operational personnel on staff. Carriers now want direct relationships with their engineering and construction vendors and have visibility into the quality of their staff, operational processes and procedures. A number of regional contractors are taking business from the major E&C contractors as a result of this trend.

• Ability to Hire Talent and Maintain Crews. There is a severe shortage of trained and certified, RF engineers and technicians (i.e. “tower climbers”) as well as experienced crew managers. The discipline applied and investments made on training and retention programs of key staff and gray collar technical talent will drive significant long-term value among these companies.

• Ability to Scale and Manage Regionally. While the wireless carriers are focused on local management and control, those vendors who can expand within region and out-of-region as customers seek greater coverage will likely see significant revenue growth opportunities. We expect the more successful and skilled wireless infrastructure providers to be acquisitive of the smaller sub-scale players who may have good crews, or a particular market presence that might be of value.

• Systems, Training and Safety. In addition to back office infrastructure and integration into customer systems, sophisticated training and safety programs are absolutely essential. Tower climbing is a very dangerous business; a culture of ‘safety first’ is the highest priority for the companies as well as the customers and tower site owners.

Some carriers fared better than others in their rollouts. Verizon Wireless has reportedly fared better because it had traditionally self-managed its local and regional contractors. Many in the industry believe this focus and control at the local level was a key to VZW’s successful deployment of the first national 4G footprint. T-Mobile was at the other extreme as it had a virtual sole source/ turnkey relationship with Nokia-Siemens Networks.

M&A and Investment Trends

Other than the major E&C conglomerates (Bechtel, B&V, Jacobs, Mastec and Dycom), several specialty engineering and technical firms operate at sizeable scale (>$250 million in revenue) Mycom is a diversified network management, OSS and engineering firm with serving carriers in the UK, Middle East, several Asian markets and the US.

Goodman was founded in 2000 and has grown rapidly with lucrative outsourcing contracts with AT&T Mobility. Its revenue peaked in 2011 at over $780 million but declined 17% in 2012 after losing several turf contracts with AT&T. The company has moved aggressive to diversify its customer base and in 2013 and spent over $150 million to acquire Multiband Inc. and Cellular Services (CSI). Multiband is a leading provider of multi-dwelling (MDU) and residential wireless infrastructure and the primary contractor to DIRECT TV. CSI is a small provider of DAS solutions primarily in the northeast. Goodman borrowed $105 million in to execute these transactions and is looking at small cell and DAS as their growth strategies. The company is now substantially leveraged ($220 million in debt) and operating at near breakeven so it is unclear these deals with payoff for Goodman.

In addition to the national and global and midsized engineering and construction firms noted above, we estimate there are approximately 50+ small- to mid–sized specialty infrastructure contractors (with annual revenue between $5 million and $250 million) in the US. Most are private and many are family-owned enterprises. Some could have as few as 50 employees and some as many as 2,000. They are most often regionally- focused, typically serving the carriers or utilities in a local region or metropolitan area. We believe the cyclical and investment trends noted above combined with the fact that the larger industry players are aggressively seeking growth will help maintain valuation multiples at historic levels. In addition to the operational characteristics described above, key drivers of value include: (i) the quality and diversity of the relationship with the wireless carriers with specific emphasis on the direct relationships; (ii) capabilities in Small Cell and DAS technologies (iii) number of experienced crews to include qualified installation engineers and tower technicians with current safety and training certifications; (iv) the extent and length of current contract backlog, and (v) top management’s quality and retention.

While there are dozens of companies we could profile, we have identified several examples of dynamic high growth middle market companies in this sector with excellent management teams and solutions portfolios. These companies include Velocitel (southern California/Virginia), SAC Wireless (Chicago/Midwest), Telkore (Pennsylvania), and Tempest Telecom (California).

Velocitel is a multi regional wireless engineering firm backed by private equity firm Willis Stein. Our research indicates revenue in the $50 to $100 million serving all the major carriers including Verizon Wireless, AT&T Mobility, Comcast, T-Mobile, Crown Castle and others. In addition to a full suite of RF engineering services, Velocitel is also diversified in the renewable energy / solar space.

SAC Wireless is a well-managed Chicago area firm with a focus on the Midwest and North Central US. Its key customers include AT&T, Sprint, Clearwire and Verizon and serves a number of OEMs and tower companies. The company is backed by private equity from Hall Capital and Everett Dobson’s investment arm (former Chairman- Dobson Cellular; now part of AT&T Mobility). The company’s is growing rapidly with an estimated revenue run rate of $60 to $90 million range per year. The company recently won a large Turf contract with a Tier 1 carrier. It offers a full portfolio of RF and DAS solutions. SAC also launched an innovative outsourced site management product known as its ‘Engine Room solution’ that has been implemented and well received by several key customers.

Tempest Telecom is a California based specialty small cell and DAS solutions company that has been evolving rapidly from a telecom equipment reseller to enterprise solutions provider to wireless carriers such as AT&T, PG&E and Verizon Wireless. We estimate the company’s annual revenue in the range $50 to $60 million with approximately 160 employees. We believe this revenue includes sizeable equipment resale as their solutions are sold and often managed on a turnkey basis. With growing demand for small cell and DAS technologies, we anticipate Tempest will be a strategic partnering target at some point.

Telkore is an example of a small regional wireless infrastructure services company. Based near Harrisburg PA, its customer base is very diversified with contracts with AT&T and a number of the large turf vendors such as Bechtel, Mastec and B&V as well as tower companies such as Crown Castle. The company is backed by private equity firm- SJF Ventures. It has growing revenue in the $10 to $15 million range. Again, as customers seek self-perform vendors, companies like Telkore will be more valuable.

DAS and & Tower Company Activity

In May 2012, the largest DAS pure play company- NextG Networks, was acquired by Crown Castle for $1.0 billion. ExteNet Systems is another large player with thousands of DAS nodes. It has major private equity backing and a $128 million investment from tower company, SBA Communications. The tower providers view DAS as a natural extension and potential threat to their core macro cell management businesses. Engineering services firm Goodman Networks acquired the small DAS company Cellular Specialists for $35 million in March 2013 indicating this will be an important line of business for the general wireless infrastructure service providers. There remains a large number of boutique DAS companies (e.g. Tempest Telecom) that provide the small cell technology as well as the installation and maintenance of turnkey DAS systems. Virtually all the E&C companies have a DAS division or have acquired companies that specialize in these deployments. DAS solutions remain a critical high growth segment of the industry. We expect considerable consolidation among the 40 plus small DAS specialty firms to continue over the next few years

Specialty Wireline Contractors

While the growth is not as dramatic as wireless infrastructure, there is continuing demand for specialty wireline services include among other things: outside fiber cable trenching, fiber optic splicing, fiber to the node (FTTN) or to the home (FTTH), fiber to the cell site (FTTCS) deployment, satellite TV installation and central office engineering, furnishing and installation. In the utility sector, critical services include transmission line deployment, substation upgrade and emergency response. The suppliers serving this segment are larger Turf Vendors led by several large and diversified public companies including Mastec, Pike Electric, MYR Group, Quanta, Henkels & McCoy, Willbros Group, Black & Veatch. DH Blattner & Sons and M.A Mortenson & Co. Other sizeable engineering companies that have exclusive EF&I³ work with such telecommunications companies include Telamon, AFL and ADC/Tyco.

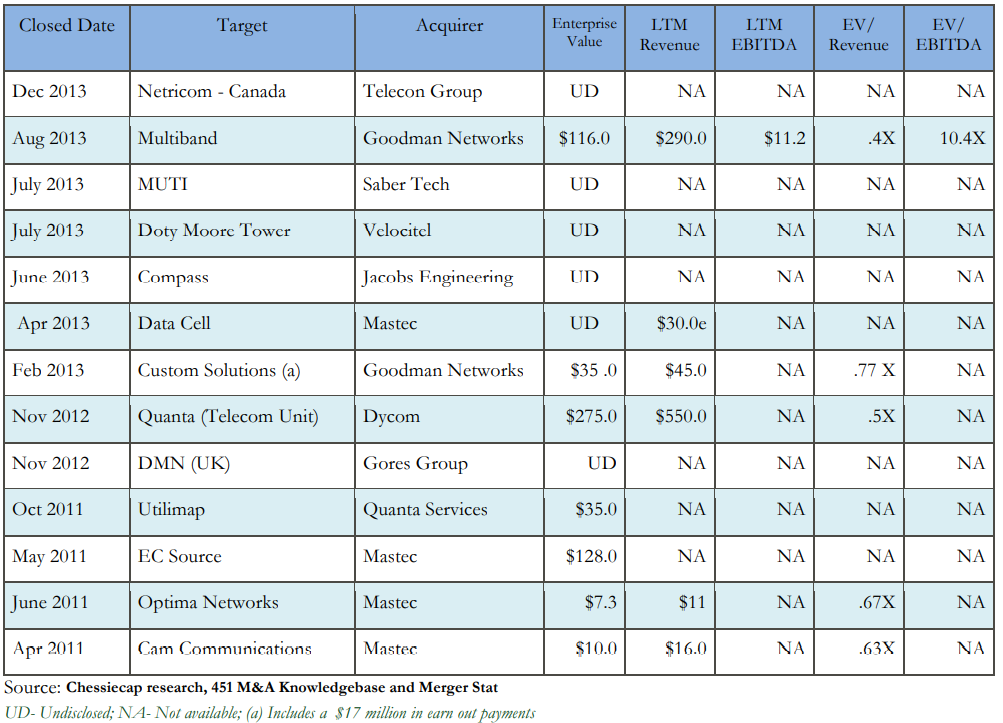

The following are recent acquisition transaction we observed over the past three years.

Recent Transactions ($ MMs)

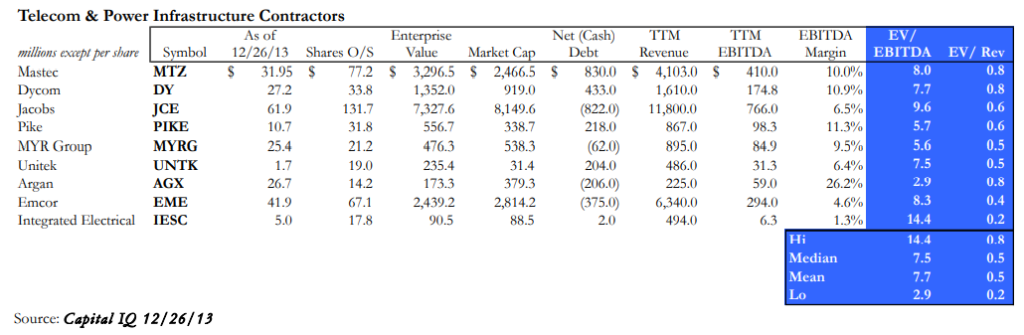

We see significant consolidation activity in the telecommunications infrastructure services segment in 2014 and 2015. The key drivers will continue to be the ability to self-perform and maintain direct contractual relationships with wireless carriers and tower companies. The ability to maintain skilled crew managers, engineers and skilled certified technicians able to keep up with evolving wireless technologies will also be of significant strategic value. We expect continuing interest in those companies that have experience and expertise in DAS and other small cell technologies. While each situation will be unique, we think premiums for high revenue growth rates and significant prime contract backlog will be at historic highs. For these companies, we see enterprise valuation ranges in the high end of the .6 to 1.0 times revenue range or 8 to 11 times EBITDA, depending on the circumstances.

Footnotes

¹IBIS World market size estimate – March 2013

²Pew Research MarketingLand Smartphone ownership in the US, July 5, 2013

³Lightwave Media, PennWall Publishing October, 2013

Investment Banking from Chessiecap Securities

Chessiecap Securities, Inc. is a boutique investment banking firm serving the needs of growth and technology companies. Our mission is to further the capital markets objectives of our clients. Our firm is a FINRA registered Broker-Dealer.

Chessiecap was founded to bring Wall Street experience to middle market companies. Our professionals provide unmatched transaction and strategic experience to our clients.

Our primary services include:

- Raising private capital

- Mergers and acquisitions

- Strategic advice to achieve capital markets transactions

- Fairness opinions and valuations

Our transaction experience focused technology-related companies:

- Information Technology

- Telecommunications

- Government Services

- Information Security

- Media & Content

- Internet Infrastructure

- Software

- Healthcare IT

- Sustainable/Clean Technologies